WF : Every market cycle, we see peak retail investor interest for equity funds almost coinciding with what we later discover was a market top. We keep talking about the need to break this cycle - to get retail investors into equity sooner in the cycle rather than at the end of it - but we have thus far not made material progress. What should AMCs and distributors do differently; if we have to genuinely help retail investors create wealth?

Aashish : The only solution is to focus on asset allocation. By asset allocation I don't mean AMCs should launch asset allocation funds; I mean to say AMCs need to allow distributors and advisors to focus on client's asset allocation. The cycle we need to break is not the market cycle and timing of our product recommendations; the cycle we actually need to break is presented as under:

CURRENT CYCLE

IDEAL CYCLE

Instead of allowing the investor and the distributor to focus on asset allocation; our industry has this weird habit of jumping schizophrenically from one idea to other depending on what AMCs believe will work in the short term. Till the AMCs are dictating the selling and the focus does not become client centric, we will not be able to break the cycle.

WF : Experts often rue the fact the FIIs have been buying consistently at cheap valuations, what domestic investors have been selling in distress. How should we get our investors to re-orient their outlook and become "smart investors" - like perhaps FIIs?

Aashish : Through the downturn and subsequent recovery in our markets i.e. from 2008 till now; FII holding in the Nifty has gone up from about 16% to 22% while public holding has gone down. The global financial crisis originated in the US as a result of which FIIs sold in India in 2008 but when the dust settled and the time came to re-allocate monies, all in all they invested more than what they withdrew from our markets. On the other hand, in a reaction to the very same financial crisis, Indians sold out of Indian equities and we are yet to get back meaningfully into the markets after that episode. So the first learning is to have belief in the Indian growth story. The Indian market definitely depends on FII money for capital flows and liquidity. But let us not forget that liquidity chases fundamentals and not the other way round. We find ourselves in a situation today where as a people we are contributing to India's growth through consumption and productivity but we are not participating in the growth by owning it. Equity has always been presented as an asset class to earn more returns but it really needs to be presented as an asset class that creates wealth and expresses patriotism at the same time. "Benefit from India's growth" should rather be "Own India's growth".

The other big issue is that there is huge fascination to buy low and sell high and to buy cheap. Our learning is that since "there is no free lunch" good quality companies are generally not cheap and they trade cheap only when markets are in distress and no one is willing to buy i.e. days when there is blood on the street. Under normal circumstances what is available cheap is generally low quality and if you buy low quality you should know when to sell. That again is a difficult skill to possess and hence we believe in our portfolio construction that one must practice BUY RIGHT : SIT TIGHT with a high quality portfolio. Usually we have seen that when people buy right they book profits and when they buy wrong they sit tight! Quite ironic but its true. FIIs have consistently bought the best quality companies in India where locals in their quest for buying cheap have been buyers of low quality companies. This is clearly manifested in the fact that FIIs hold more proportion of Nifty vis-Ã -vis their holding of CNX 500 while domestic investors own more of CNX 500 than in Nifty.

WF : In what ways must distributors reframe investor thinking to get them to actually "Buy Right and Sit Tight"?

Aashish : I found some very interesting thoughts in this book called "The Excellent Investment Advisor" written by Nick Murray. He says that since investors are always fearful of investing and staying invested in equities we need to make them understand how negative developments in equity markets are actually to be viewed as opportunities to create wealth.

We firmly believe at Motilal Oswal AMC that wealth is created by buying good quality companies and holding on to them. But it is the market behavior and investors reactions to the same that prevents the BUY RIGHT : SIT TIGHT phenomenon from playing to its potential. Following thoughts from the book are worth educating investors on:

A major price decline.....

.....is a rally in Value and Yield

If the declines went away.....

.....the returns would go away

If you haven't finished buying yet.....

.....why do you want market to go up ?

WF : You are very bullish about a coming wave of domestic flows into equity markets. What underpins this confidence?

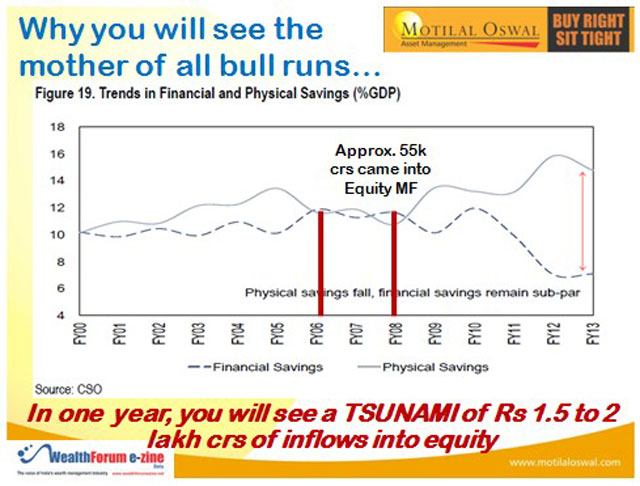

Aashish : India is known to be a nation of savers and savings are broadly dividend into physical and financial savings. Past history shows that when real interest rates are negative (interest rates lower than inflation) people would not find it rewarding to make financial savings. This explains why Indians have preferred gold and land over the last five years when inflation was very high.

One particular period when real rates were positive in 2007 resulted in a gigantic 1% of GDP kind of inflow into equity MFs alone. FY2015 is a year when real rates seem to be turning positive and we are already seeing early signs of a sustained flow into equities. If we again get 1% of GDP this will result in nearly Rs 1.5 lac crs of inflows into equity MFs. This is bound to happen for certain as financial savings overtake physical savings in this year and possibly even the next.

WF : How does your AMC propose to make the most of this business cycle? What can your distributors expect from Motilal Oswal MF?

Aashish : Motilal Oswal AMC is a specialist equity house and we are fully geared to leverage on the market scenario. Distributors will find steady and consistent communication on equities irrespective of whether Nifty is at 8000 or 10000 or 6000! We manage only equity portfolios by way of our market leading PMS and now our suite of 3 open ended NO LOAD equity funds. With one focused investment philosophy we do not have any distraction of multiple types of funds to manage and promote and we do not have distraction of asset classes other than equities. We are a "small" AMC but let me tell you, with total over Rs 3000 crs of equity assets under management not so "small". We are "small" by design because we would like to offer a limited range of products based on our core competency of wealth creation.

There is huge skin in the game because as a group of equity investors, Motilal Oswal Financial Services Group invests all of its proprietary investment into the very same equity mutual fund schemes where we are canvassing for investors monies. At the time of writing this, out of an open ended equity MF corpus of Rs 825 crs, almost Rs 450 crs of assets are proprietary in nature i.e. our own group money from promoters, sponsors and various corporate entities linked to MOFSL group.

Over the number of years, investors' allocation has been concentrated with very few AMCs especially when it comes to equity investing due to lack of enough number of reliable and sustainable options. Motilal Oswal as a group has been living and breathing equities and equities only since 1987 and we are in a position to offer a viable alternative to advisors and distributors for fulfilling their client's equity allocation. We run highly focused portfolios of 15 to 20 stocks with a buy and hold approach. I am saying a viable alternative because usually when a new AMC comes with their equity products, they may not have a tried and tested method of investing in form of a stated investment philosophy. In this aspect Motilal Oswal AMC is unique. We have a tried and tested investment philosophy in form of BUY RIGHT : SIT TIGHT. It has worked for us in our market leading PMS business over the last 12 years where we manage nearly Rs 2000 crs.

Share this article